Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeLSTM Architecture for Oil Stocks Prices Prediction

Paper and Code

Jan 02, 2022

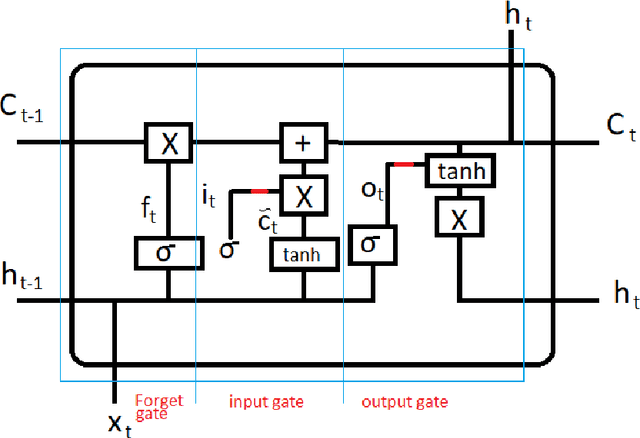

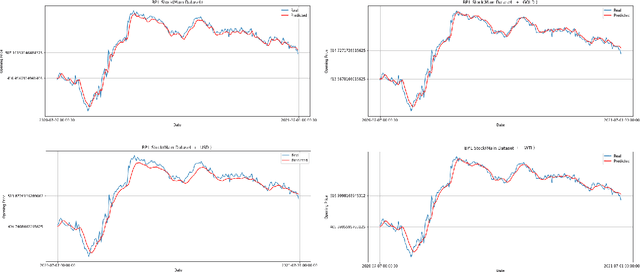

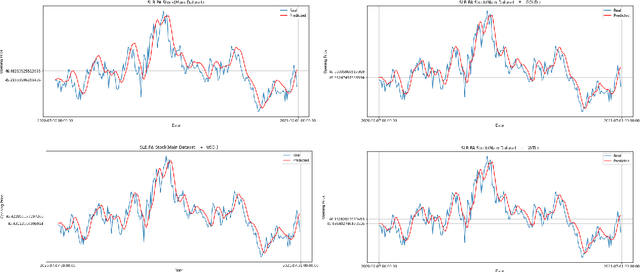

Oil companies are among the largest companies in the world whose economic indicators in the global stock market have a great impact on the world economy and market due to their relation to gold, crude oil, and the dollar. To quantify these relations we use the correlation feature and the relationships between stocks with the dollar, crude oil, gold, and major oil company stock indices, we create datasets and compare the results of forecasts with real data. To predict the stocks of different companies, we use Recurrent Neural Networks (RNNs) and LSTM, because these stocks change in time series. We carry on empirical experiments and perform on the stock indices dataset to evaluate the prediction performance in terms of several common error metrics such as Mean Square Error (MSE), Mean Absolute Error (MAE), Root Mean Square Error (RMSE), and Mean Absolute Percentage Error (MAPE). The received results are promising and present a reasonably accurate prediction for the price of oil companies' stocks in the near future. The results show that RNNs do not have the interpretability, and we cannot improve the model by adding any correlated data.