Get our free extension to see links to code for papers anywhere online!Free add-on: code for papers everywhere!Free add-on: See code for papers anywhere!

Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeLearning from multivariate discrete sequential data using a restricted Boltzmann machine model

Paper and Code

Apr 28, 2018

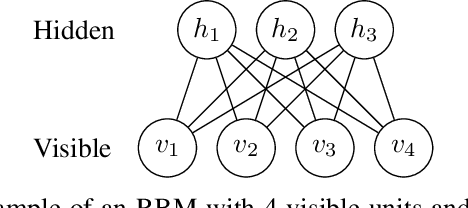

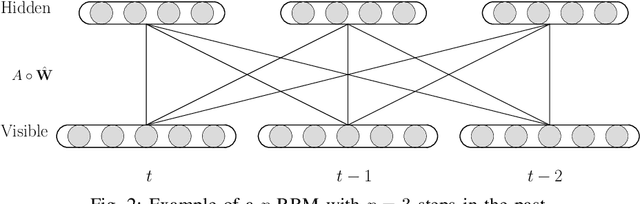

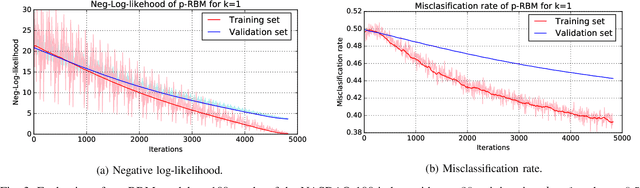

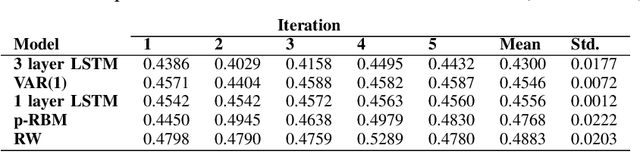

A restricted Boltzmann machine (RBM) is a generative neural-network model with many novel applications such as collaborative filtering and acoustic modeling. An RBM lacks the capacity to retain memory, making it inappropriate for dynamic data modeling as in time-series analysis. In this paper we address this issue by proposing the p-RBM model, a generalization of the regular RBM model, capable of retaining memory of p past states. We further show how to train the p-RBM model using contrastive divergence and test our model on the problem of predicting the stock market direction considering 100 stocks of the NASDAQ-100 index. Obtained results show that the p-RBM offer promising prediction potential.

* 6 pages, 3 figures, Accepted as conference paper in IEEE-COLCACI 2018

View paper on