Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeLabel Augmentation via Time-based Knowledge Distillation for Financial Anomaly Detection

Paper and Code

Jan 05, 2021

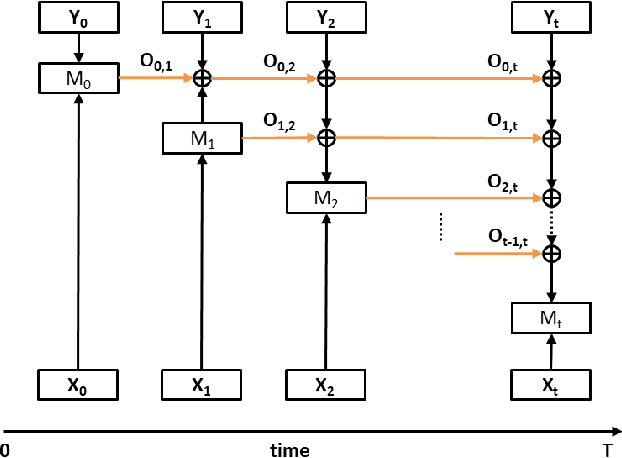

Detecting anomalies has become increasingly critical to the financial service industry. Anomalous events are often indicative of illegal activities such as fraud, identity theft, network intrusion, account takeover, and money laundering. Financial anomaly detection use cases face serious challenges due to the dynamic nature of the underlying patterns especially in adversarial environments such as constantly changing fraud tactics. While retraining the models with the new patterns is absolutely essential; keeping up with the rapid changes introduces other challenges as it moves the model away from older patterns or continuously grows the size of the training data. The resulting data growth is hard to manage and it reduces the agility of the models' response to the latest attacks. Due to the data size limitations and the need to track the latest patterns, older time periods are often dropped in practice, which in turn, causes vulnerabilities. In this study, we propose a label augmentation approach to utilize the learning from older models to boost the latest. Experimental results show that the proposed approach provides a significant reduction in training time, while providing potential performance improvement.