Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeInflation forecasting with attention based transformer neural networks

Paper and Code

Mar 29, 2023

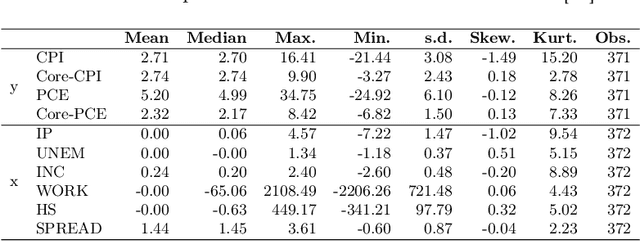

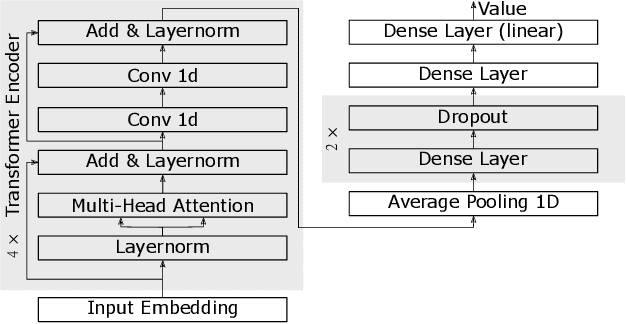

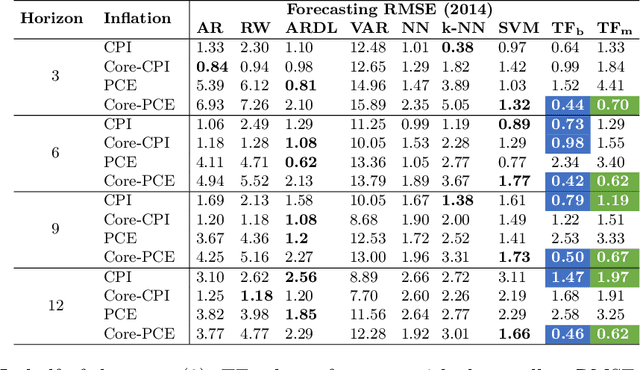

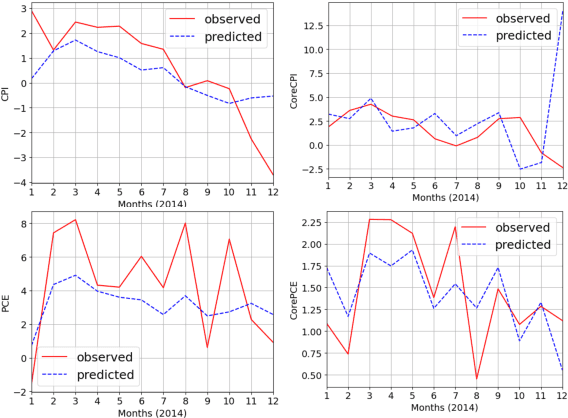

Inflation is a major determinant for allocation decisions and its forecast is a fundamental aim of governments and central banks. However, forecasting inflation is not a trivial task, as its prediction relies on low frequency, highly fluctuating data with unclear explanatory variables. While classical models show some possibility of predicting inflation, reliably beating the random walk benchmark remains difficult. Recently, (deep) neural networks have shown impressive results in a multitude of applications, increasingly setting the new state-of-the-art. This paper investigates the potential of the transformer deep neural network architecture to forecast different inflation rates. The results are compared to a study on classical time series and machine learning models. We show that our adapted transformer, on average, outperforms the baseline in 6 out of 16 experiments, showing best scores in two out of four investigated inflation rates. Our results demonstrate that a transformer based neural network can outperform classical regression and machine learning models in certain inflation rates and forecasting horizons.