Get our free extension to see links to code for papers anywhere online!Free add-on: code for papers everywhere!Free add-on: See code for papers anywhere!

Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeFinancial Time Series Data Processing for Machine Learning

Paper and Code

Jul 03, 2019

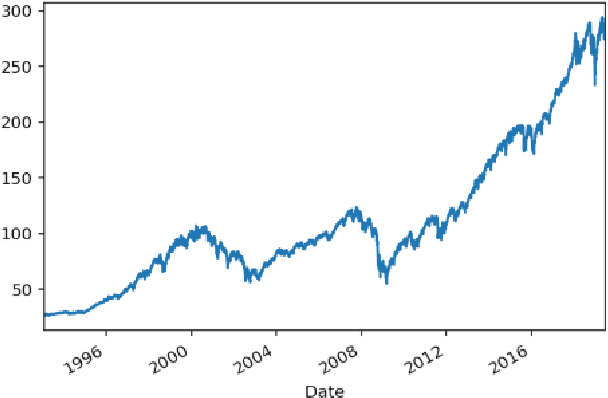

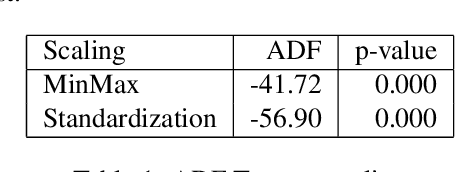

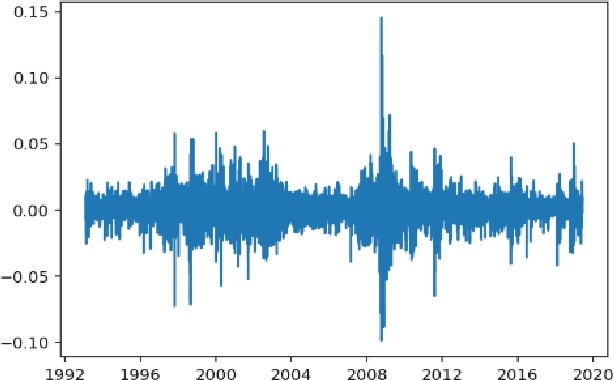

This article studies the financial time series data processing for machine learning. It introduces the most frequent scaling methods, then compares the resulting stationarity and preservation of useful information for trend forecasting. It proposes an empirical test based on the capability to learn simple data relationship with simple models. It also speaks about the data split method specific to time series, avoiding unwanted overfitting and proposes various labelling for classification and regression.

View paper on