Get our free extension to see links to code for papers anywhere online!Free add-on: code for papers everywhere!Free add-on: See code for papers anywhere!

Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeEstimation of scale functions to model heteroscedasticity by support vector machines

Paper and Code

Nov 08, 2011

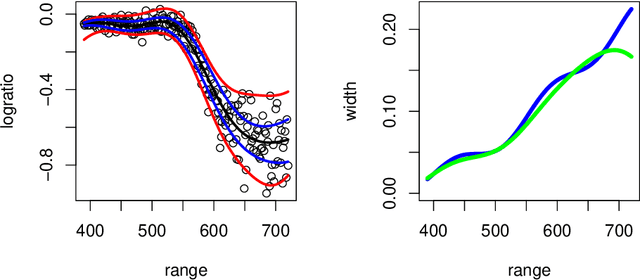

A main goal of regression is to derive statistical conclusions on the conditional distribution of the output variable Y given the input values x. Two of the most important characteristics of a single distribution are location and scale. Support vector machines (SVMs) are well established to estimate location functions like the conditional median or the conditional mean. We investigate the estimation of scale functions by SVMs when the conditional median is unknown, too. Estimation of scale functions is important e.g. to estimate the volatility in finance. We consider the median absolute deviation (MAD) and the interquantile range (IQR) as measures of scale. Our main result shows the consistency of MAD-type SVMs.

View paper on