Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeDynamic cyber risk estimation with Competitive Quantile Autoregression

Paper and Code

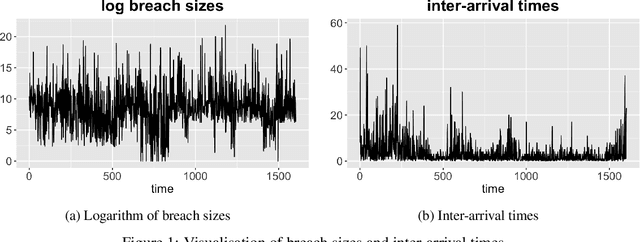

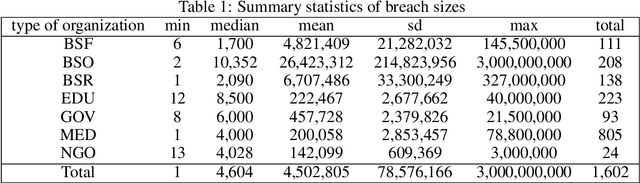

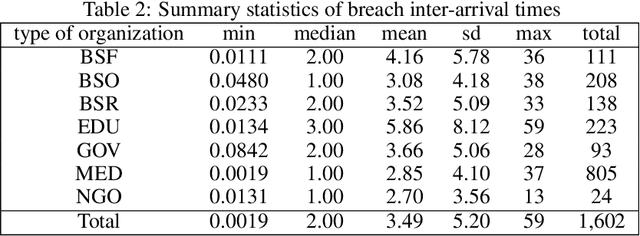

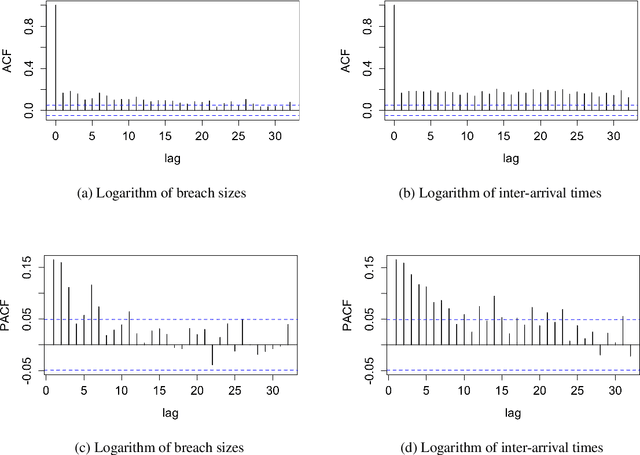

Cyber risk estimation is an essential part of any information technology system's design and governance since the cost of the system compromise could be catastrophic. An effective risk framework has the potential to predict, assess, and mitigate possible adverse events. We propose two methods for modelling Value-at-Risk (VaR) which can be used for any time-series data. The first approach is based on Quantile Autoregression (QAR), which can estimate VaR for different quantiles, i.e. confidence levels. The second method, called Competitive Quantile Autoregression (CQAR), dynamically re-estimates cyber risk as soon as new data becomes available. This method provides a theoretical guarantee that it asymptotically performs as well as any QAR at any time point in the future. We show that these methods can predict the size and inter-arrival time of cyber hacking breaches by running coverage tests. The proposed approaches allow to model a separate stochastic process for each significance level and therefore provide more flexibility compared to previously proposed techniques. We provide a fully reproducible code used for conducting the experiments.