Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeDual reparametrized Variational Generative Model for Time-Series Forecasting

Paper and Code

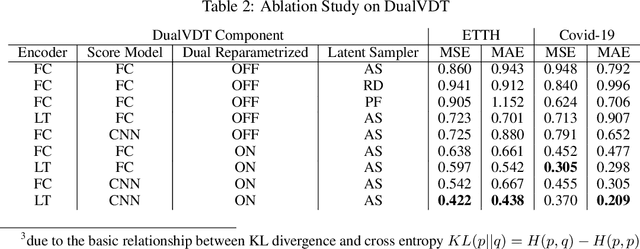

This paper propose DualVDT, a generative model for Time-series forecasting. Introduced dual reparametrized variational mechanisms on variational autoencoder (VAE) to tighter the evidence lower bound (ELBO) of the model, prove the advance performance analytically. This mechanism leverage the latent score based generative model (SGM), explicitly denoising the perturbation accumulated on latent vector through reverse time stochastic differential equation and variational ancestral sampling. The posterior of denoised latent distribution fused with dual reparametrized variational density. The KL divergence in ELBO will reduce to reach the better results of the model. This paper also proposed a latent attention mechanisms to extract multivariate dependency explicitly. Build the local temporal dependency simultaneously in factor wised through constructed local topology and temporal wised. The proven and experiment on multiple datasets illustrate, DualVDT, with a novel dual reparametrized structure, which denoise the latent perturbation through the reverse dynamics combining local-temporal inference, has the advanced performance both analytically and experimentally.