Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeDoes non-linear factorization of financial returns help build better and stabler portfolios?

Paper and Code

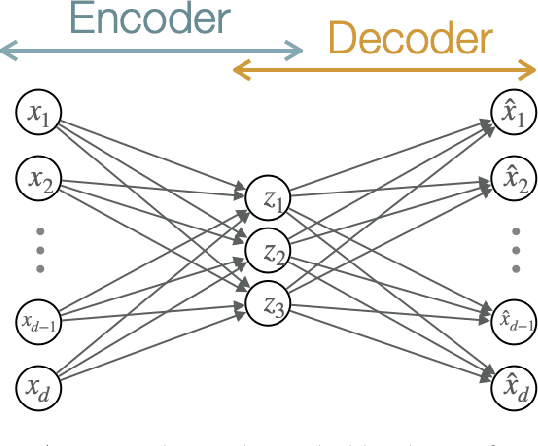

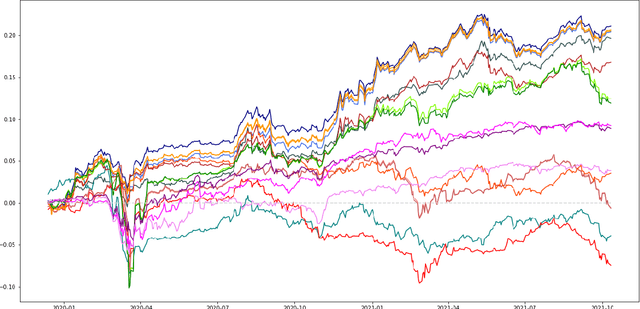

A portfolio allocation method based on linear and non-linear latent constrained conditional factors is presented. The factor loadings are constrained to always be positive in order to obtain long-only portfolios, which is not guaranteed by classical factor analysis or PCA. In addition, the factors are to be uncorrelated among clusters in order to build long-only portfolios. Our approach is based on modern machine learning tools: convex Non-negative Matrix Factorization (NMF) and autoencoder neural networks, designed in a specific manner to enforce the learning of useful hidden data structure such as correlation between the assets' returns. Our technique finds lowly correlated linear and non-linear conditional latent factors which are used to build outperforming global portfolios consisting of cryptocurrencies and traditional assets, similar to hierarchical clustering method. We study the dynamics of the derived non-linear factors in order to forecast tail losses of the portfolios and thus build more stable ones.