Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeDensity-Calibrated Conformal Quantile Regression

Paper and Code

Dec 02, 2024

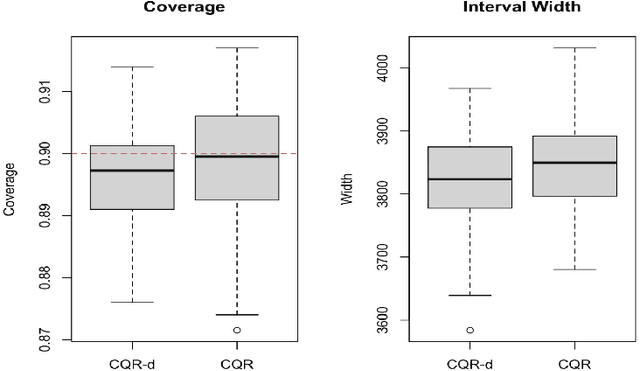

This paper introduces the Density-Calibrated Conformal Quantile Regression (CQR-d) method, a novel approach for constructing prediction intervals that adapts to varying uncertainty across the feature space. Building upon conformal quantile regression, CQR-d incorporates local information through a weighted combination of local and global conformity scores, where the weights are determined by local data density. We prove that CQR-d provides valid marginal coverage at level $1 - \alpha - \epsilon$, where $\epsilon$ represents a small tolerance from numerical optimization. Through extensive simulation studies and an application to the a heteroscedastic dataset available in R, we demonstrate that CQR-d maintains the desired coverage while producing substantially narrower prediction intervals compared to standard conformal quantile regression (CQR). The method's effectiveness is particularly pronounced in settings with clear local uncertainty patterns, making it a valuable tool for prediction tasks in heterogeneous data environments.