Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeDeepVARwT: Deep Learning for a VAR Model with Trend

Paper and Code

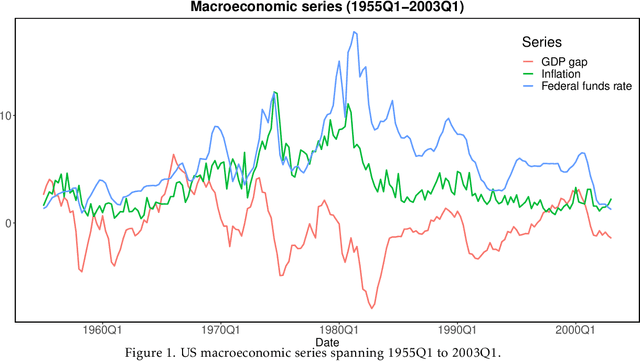

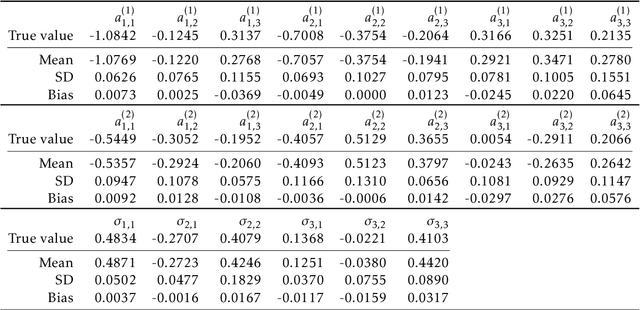

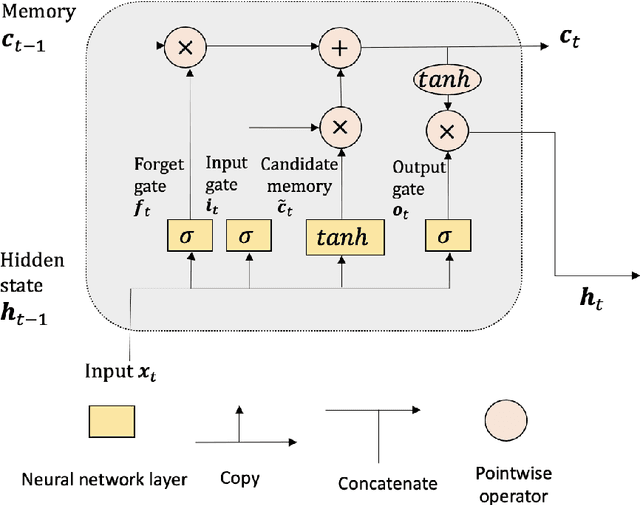

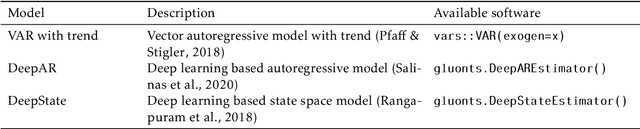

The vector autoregressive (VAR) model has been used to describe the dependence within and across multiple time series. This is a model for stationary time series which can be extended to allow the presence of a deterministic trend in each series. Detrending the data either parametrically or nonparametrically before fitting the VAR model gives rise to more errors in the latter part. In this study, we propose a new approach called DeepVARwT that employs deep learning methodology for maximum likelihood estimation of the trend and the dependence structure at the same time. A Long Short-Term Memory (LSTM) network is used for this purpose. To ensure the stability of the model, we enforce the causality condition on the autoregressive coefficients using the transformation of Ansley & Kohn (1986). We provide a simulation study and an application to real data. In the simulation study, we use realistic trend functions generated from real data and compare the estimates with true function/parameter values. In the real data application, we compare the prediction performance of this model with state-of-the-art models in the literature.