Get our free extension to see links to code for papers anywhere online!Free add-on: code for papers everywhere!Free add-on: See code for papers anywhere!

Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeDeep learning method for solving stochastic optimal control problem via stochastic maximum principle

Paper and Code

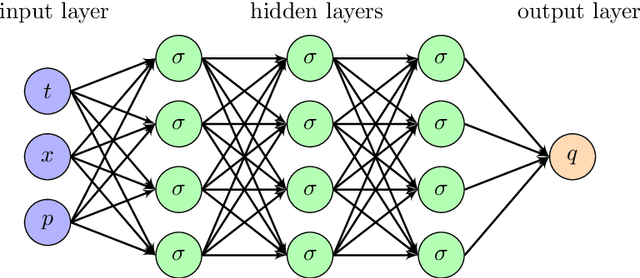

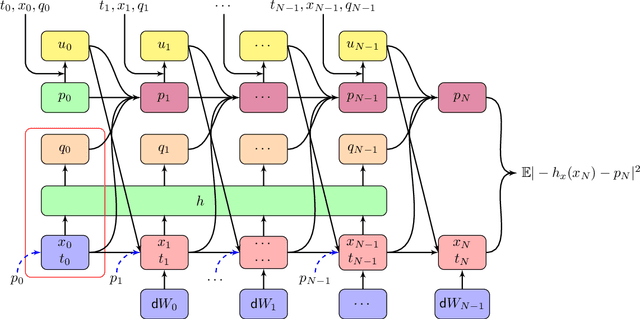

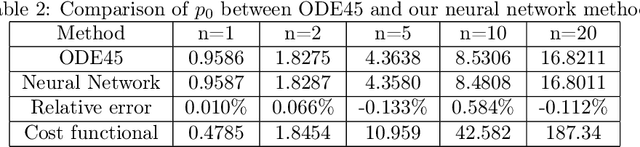

In this paper, we aim to solve the stochastic optimal control problem via deep learning. Through the stochastic maximum principle and its corresponding Hamiltonian system, we propose a framework in which the original control problem is reformulated as a new one. This new stochastic optimal control problem has a quadratic loss function at the terminal time which provides an easier way to build a neural network structure. But the cost is that we must deal with an additional maximum condition. Some numerical examples such as the linear quadratic (LQ) stochastic optimal control problem and the calculation of G-expectation have been studied.

View paper on