Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeDeep learning based Chinese text sentiment mining and stock market correlation research

Paper and Code

May 10, 2022

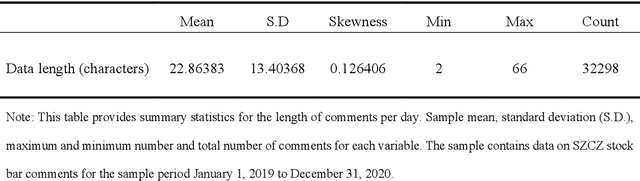

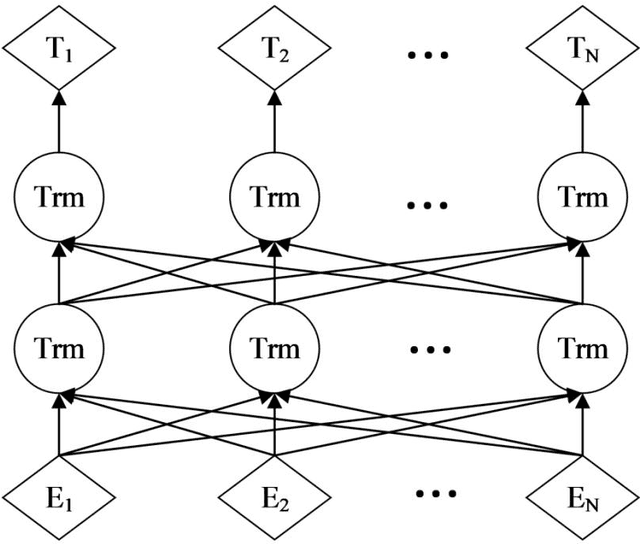

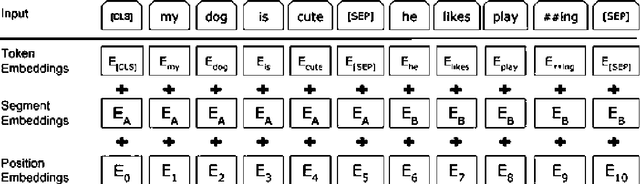

We explore how to crawl financial forum data such as stock bars and combine them with deep learning models for sentiment analysis. In this paper, we will use the BERT model to train against the financial corpus and predict the SZSE Component Index, and find that applying the BERT model to the financial corpus through the maximum information coefficient comparison study. The obtained sentiment features will be able to reflect the fluctuations in the stock market and help to improve the prediction accuracy effectively. Meanwhile, this paper combines deep learning with financial text, in further exploring the mechanism of investor sentiment on stock market through deep learning method, which will be beneficial for national regulators and policy departments to develop more reasonable policy guidelines for maintaining the stability of stock market.