Get our free extension to see links to code for papers anywhere online!Free add-on: code for papers everywhere!Free add-on: See code for papers anywhere!

Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeCalibration with Changing Checking Rules and Its Application to Short-Term Trading

Paper and Code

May 21, 2011

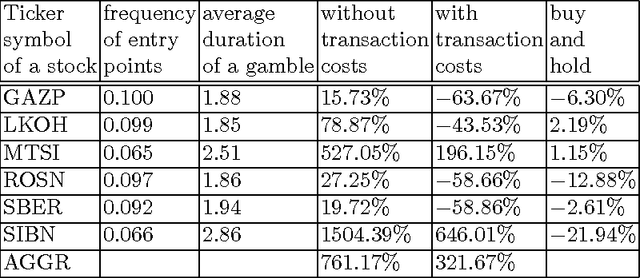

We provide a natural learning process in which a financial trader without a risk receives a gain in case when Stock Market is inefficient. In this process, the trader rationally choose his gambles using a prediction made by a randomized calibrated algorithm. Our strategy is based on Dawid's notion of calibration with more general changing checking rules and on some modification of Kakade and Foster's randomized algorithm for computing calibrated forecasts.

* 15 pages, 3 figures

View paper on