Get our free extension to see links to code for papers anywhere online!Free add-on: code for papers everywhere!Free add-on: See code for papers anywhere!

Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeApplications of multivariate quasi-random sampling with neural networks

Paper and Code

Dec 15, 2020

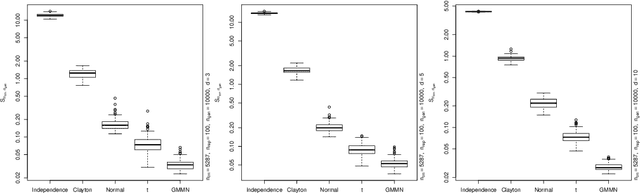

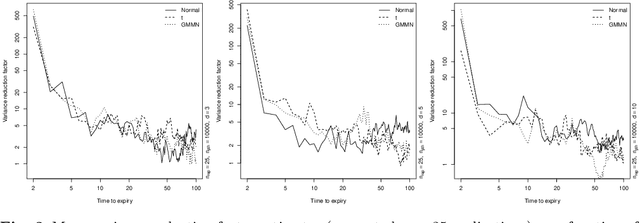

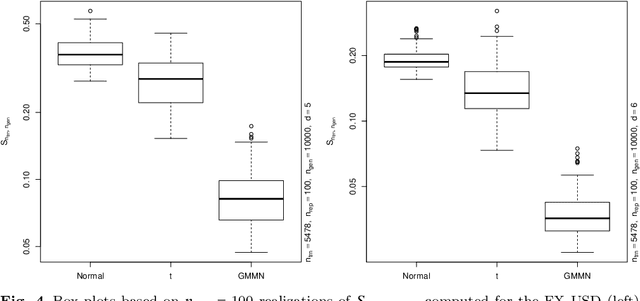

Generative moment matching networks (GMMNs) are suggested for modeling the cross-sectional dependence between stochastic processes. The stochastic processes considered are geometric Brownian motions and ARMA-GARCH models. Geometric Brownian motions lead to an application of pricing American basket call options under dependence and ARMA-GARCH models lead to an application of simulating predictive distributions. In both types of applications the benefit of using GMMNs in comparison to parametric dependence models is highlighted and the fact that GMMNs can produce dependent quasi-random samples with no additional effort is exploited to obtain variance reduction.

* 16 pages, 5 figures

View paper on