Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeAdaptive Learning on Time Series: Method and Financial Applications

Paper and Code

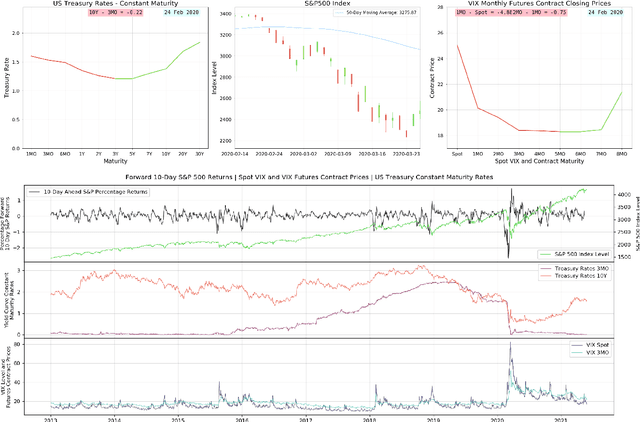

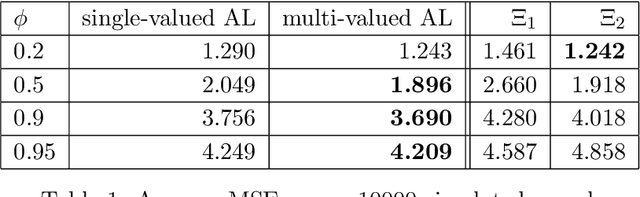

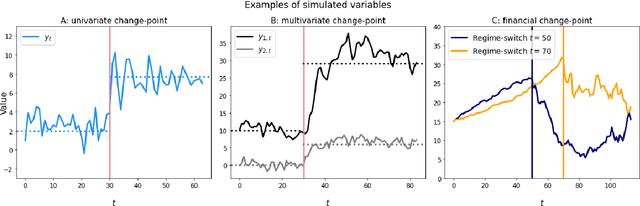

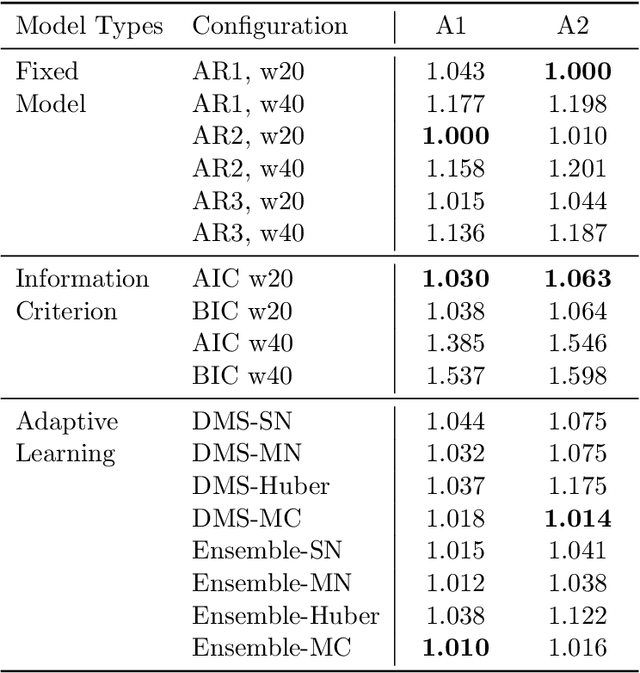

We formally introduce a time series statistical learning method, called Adaptive Learning, capable of handling model selection, out-of-sample forecasting and interpretation in a noisy environment. Through simulation studies we demonstrate that the method can outperform traditional model selection techniques such as AIC and BIC in the presence of regime-switching, as well as facilitating window size determination when the Data Generating Process is time-varying. Empirically, we use the method to forecast S&P 500 returns across multiple forecast horizons, employing information from the VIX Curve and the Yield Curve. We find that Adaptive Learning models are generally on par with, if not better than, the best of the parametric models a posteriori, evaluated in terms of MSE, while also outperforming under cross validation. We present a financial application of the learning results and an interpretation of the learning regime during the 2020 market crash. These studies can be extended in both a statistical direction and in terms of financial applications.