Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeA Residual Bootstrap for High-Dimensional Regression with Near Low-Rank Designs

Paper and Code

Jul 04, 2016

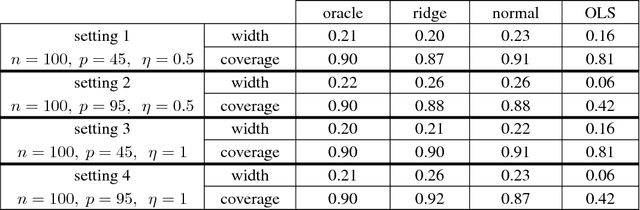

We study the residual bootstrap (RB) method in the context of high-dimensional linear regression. Specifically, we analyze the distributional approximation of linear contrasts $c^{\top} (\hat{\beta}_{\rho}-\beta)$, where $\hat{\beta}_{\rho}$ is a ridge-regression estimator. When regression coefficients are estimated via least squares, classical results show that RB consistently approximates the laws of contrasts, provided that $p\ll n$, where the design matrix is of size $n\times p$. Up to now, relatively little work has considered how additional structure in the linear model may extend the validity of RB to the setting where $p/n\asymp 1$. In this setting, we propose a version of RB that resamples residuals obtained from ridge regression. Our main structural assumption on the design matrix is that it is nearly low rank --- in the sense that its singular values decay according to a power-law profile. Under a few extra technical assumptions, we derive a simple criterion for ensuring that RB consistently approximates the law of a given contrast. We then specialize this result to study confidence intervals for mean response values $X_i^{\top} \beta$, where $X_i^{\top}$ is the $i$th row of the design. More precisely, we show that conditionally on a Gaussian design with near low-rank structure, RB simultaneously approximates all of the laws $X_i^{\top}(\hat{\beta}_{\rho}-\beta)$, $i=1,\dots,n$. This result is also notable as it imposes no sparsity assumptions on $\beta$. Furthermore, since our consistency results are formulated in terms of the Mallows (Kantorovich) metric, the existence of a limiting distribution is not required.