Get our free extension to see links to code for papers anywhere online!Free add-on: code for papers everywhere!Free add-on: See code for papers anywhere!

Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeA note on VIX for postprocessing quantitative strategies

Paper and Code

Jul 08, 2022

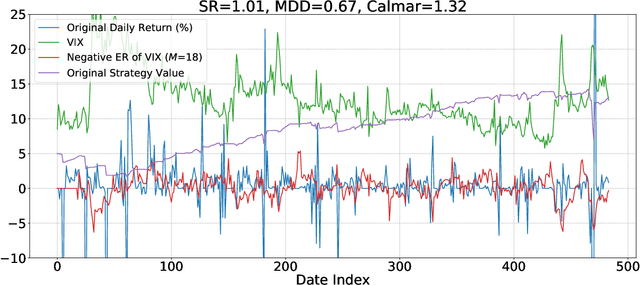

In this note, we introduce how to use Volatility Index (VIX) for postprocessing quantitative strategies so as to increase the Sharpe ratio and reduce trading risks. The signal from this procedure is an indicator of trading or not on a daily basis. Finally, we analyze this procedure on SH510300 and SH510050 assets. The strategies are evaluated by measurements of Sharpe ratio, max drawdown, and Calmar ratio. However, there is always a risk of loss in trading. The results from the tests are just examples of how the method works; no claim is made on the suggestion of real market positions.

View paper on