Get our free extension to see links to code for papers anywhere online!Free add-on: code for papers everywhere!Free add-on: See code for papers anywhere!

Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeA General Stochastic Optimization Framework for Convergence Bidding

Paper and Code

Oct 12, 2022

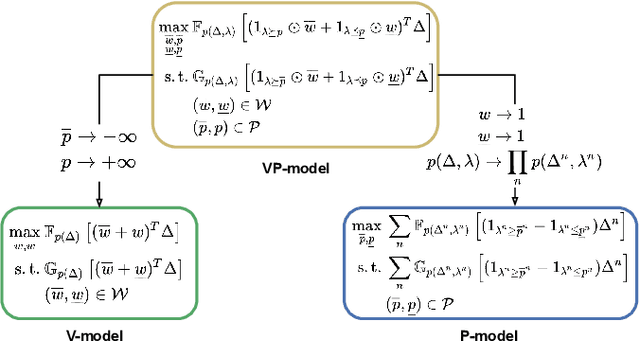

We introduce a general stochastic optimization framework to obtain optimal convergence (virtual) bid curves. Within this framework, we develop a computationally tractable linear programming-based optimization model, which produces bid prices and volumes simultaneously. We also show that different approximations and simplifications in the general model lead naturally to well-known convergence bidding approaches, such as self-scheduling and opportunistic approaches.

View paper on