Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeFrank-Wolfe-based Algorithms for Approximating Tyler's M-estimator

Jun 19, 2022

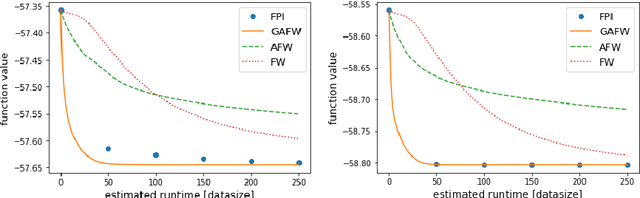

Tyler's M-estimator is a well known procedure for robust and heavy-tailed covariance estimation. Tyler himself suggested an iterative fixed-point algorithm for computing his estimator however, it requires super-linear (in the size of the data) runtime per iteration, which may be prohibitive in large scale. In this work we propose, to the best of our knowledge, the first Frank-Wolfe-based algorithms for computing Tyler's estimator. One variant uses standard Frank-Wolfe steps, the second also considers \textit{away-steps} (AFW), and the third is a \textit{geodesic} version of AFW (GAFW). AFW provably requires, up to a log factor, only linear time per iteration, while GAFW runs in linear time (up to a log factor) in a large $n$ (number of data-points) regime. All three variants are shown to provably converge to the optimal solution with sublinear rate, under standard assumptions, despite the fact that the underlying optimization problem is not convex nor smooth. Under an additional fairly mild assumption, that holds with probability 1 when the (normalized) data-points are i.i.d. samples from a continuous distribution supported on the entire unit sphere, AFW and GAFW are proved to converge with linear rates. Importantly, all three variants are parameter-free and use adaptive step-sizes.