Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeWaveCorr: Correlation-savvy Deep Reinforcement Learning for Portfolio Management

Sep 28, 2021

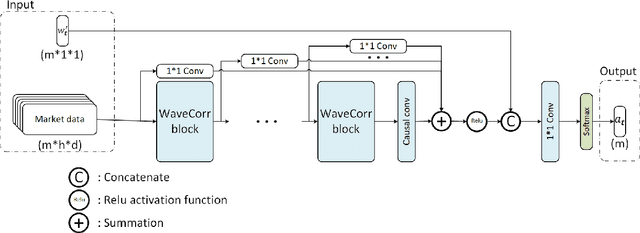

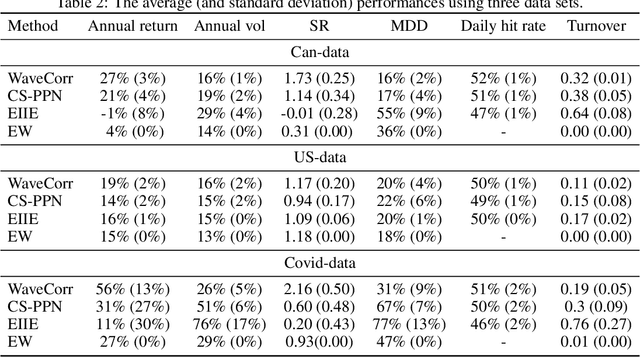

The problem of portfolio management represents an important and challenging class of dynamic decision making problems, where rebalancing decisions need to be made over time with the consideration of many factors such as investors preferences, trading environments, and market conditions. In this paper, we present a new portfolio policy network architecture for deep reinforcement learning (DRL)that can exploit more effectively cross-asset dependency information and achieve better performance than state-of-the-art architectures. In particular, we introduce a new property, referred to as \textit{asset permutation invariance}, for portfolio policy networks that exploit multi-asset time series data, and design the first portfolio policy network, named WaveCorr, that preserves this invariance property when treating asset correlation information. At the core of our design is an innovative permutation invariant correlation processing layer. An extensive set of experiments are conducted using data from both Canadian (TSX) and American stock markets (S&P 500), and WaveCorr consistently outperforms other architectures with an impressive 3%-25% absolute improvement in terms of average annual return, and up to more than 200% relative improvement in average Sharpe ratio. We also measured an improvement of a factor of up to 5 in the stability of performance under random choices of initial asset ordering and weights. The stability of the network has been found as particularly valuable by our industrial partner.