Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeSocial Media Sentiment Analysis for Cryptocurrency Market Prediction

Apr 19, 2022

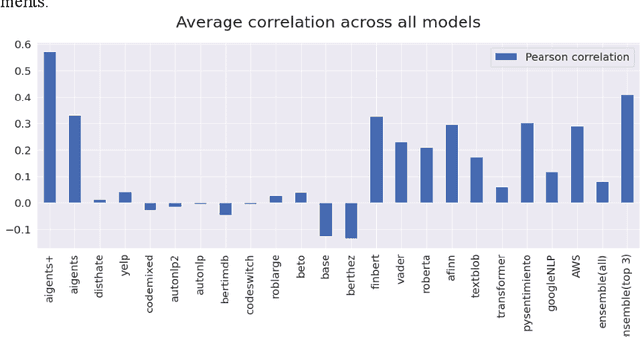

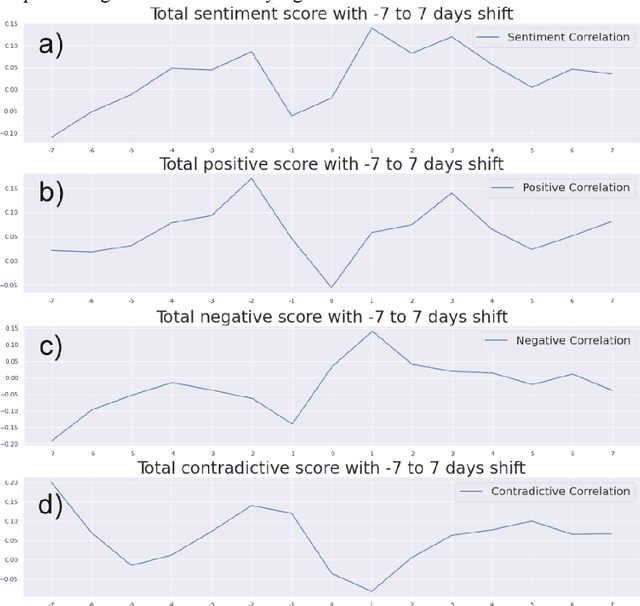

In this paper, we explore the usability of different natural language processing models for the sentiment analysis of social media applied to financial market prediction, using the cryptocurrency domain as a reference. We study how the different sentiment metrics are correlated with the price movements of Bitcoin. For this purpose, we explore different methods to calculate the sentiment metrics from a text finding most of them not very accurate for this prediction task. We find that one of the models outperforms more than 20 other public ones and makes it possible to fine-tune it efficiently given its interpretable nature. Thus we confirm that interpretable artificial intelligence and natural language processing methods might be more valuable practically than non-explainable and non-interpretable ones. In the end, we analyse potential causal connections between the different sentiment metrics and the price movements.