Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeExploring the Antecedents of Consumer Confidence through Semantic Network Analysis of Online News

May 11, 2021

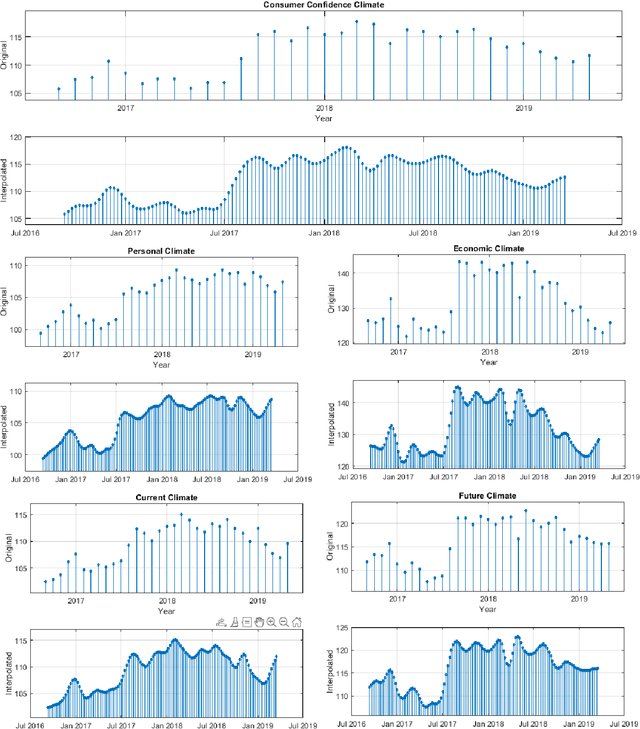

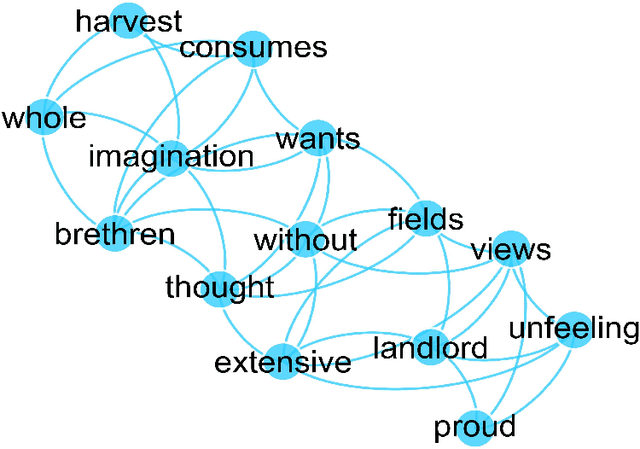

This article studies the impact of online news on social and economic consumer perceptions through the application of semantic network analysis. Using almost 1.3 million online articles on Italian media covering a period of four years, we assessed the incremental predictive power of economic-related keywords on the Consumer Confidence Index. We transformed news into networks of co-occurring words and calculated the semantic importance of specific keywords, to see if words appearing in the articles could anticipate consumers' judgements about the economic situation. Results show that economic-related keywords have a stronger predictive power if we consider the current households and national situation, while their predictive power is less significant with regards to expectations about the future. Our indicator of semantic importance offers a complementary approach to estimate consumer confidence, lessening the limitations of traditional survey-based methods.

Forecasting financial markets with semantic network analysis in the COVID-19 crisis

Sep 09, 2020

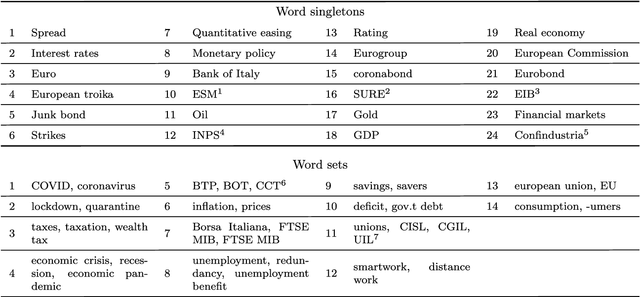

This paper uses a new textual data index for predicting stock market data. The index is applied to a large set of news to evaluate the importance of one or more general economic related keywords appearing in the text. The index assesses the importance of the economic related keywords, based on their frequency of use and semantic network position. We apply it to the Italian press and construct indices to predict Italian stock and bond market returns and volatilities in a recent sample period, including the COVID-19 crisis. The evidence shows that the index captures well the different phases of financial time series. Moreover, results indicate strong evidence of predictability for bond market data, both returns and volatilities, short and long maturities, and stock market volatility.