Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeLearning the Gap in the Day-Ahead and Real-Time Locational Marginal Prices in the Electricity Market

Dec 23, 2020

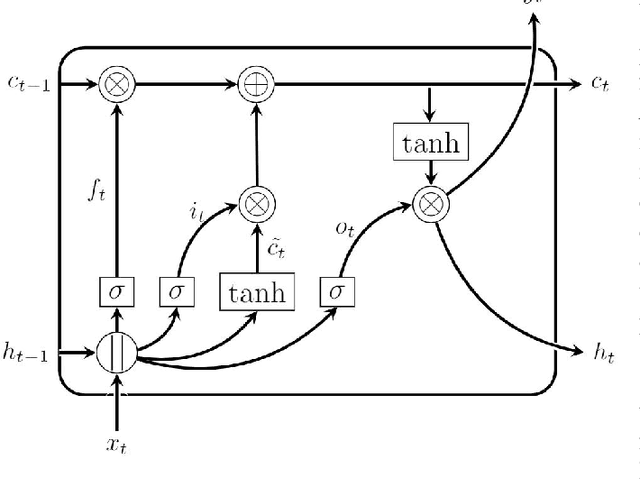

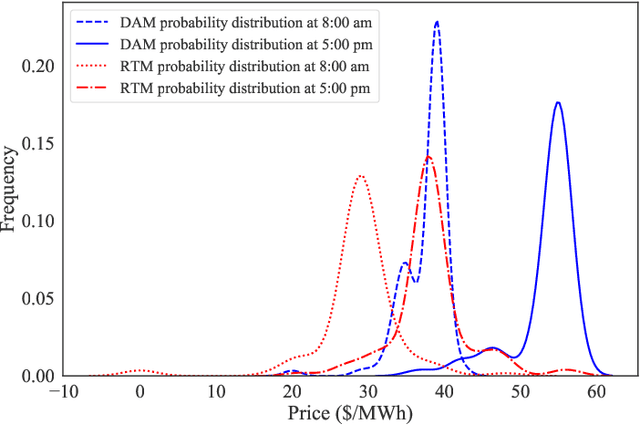

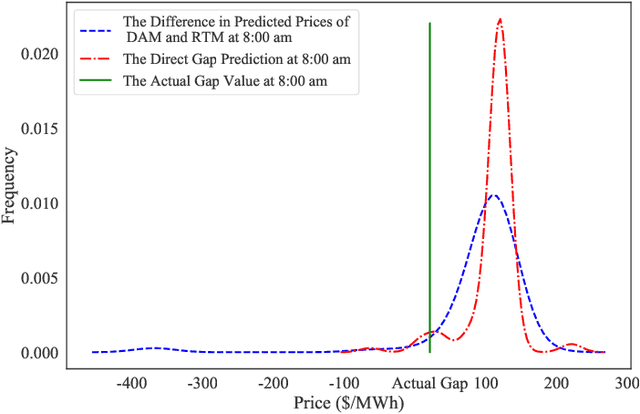

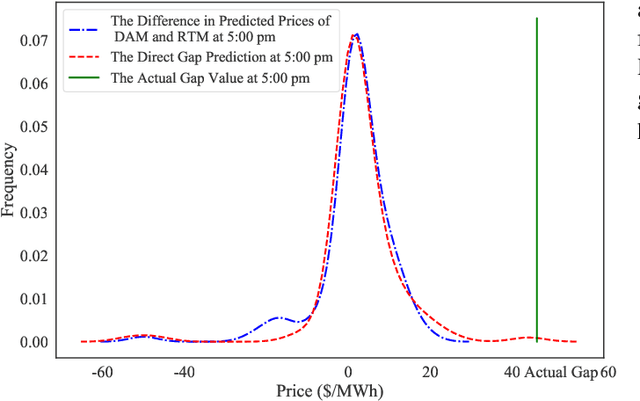

In this paper, statistical machine learning algorithms, as well as deep neural networks, are used to predict the values of the price gap between day-ahead and real-time electricity markets. Several exogenous features are collected and impacts of these features are examined to capture the best relations between the features and the target variable. Ensemble learning algorithm namely the Random Forest issued to calculate the probability distribution of the predicted electricity prices for day-ahead and real-time markets. Long-Short-Term-Memory (LSTM) is utilized to capture long term dependencies in predicting direct gap values between mentioned markets and the benefits of directly predicting the gap price rather than subtracting the predictions of day-ahead and real-time markets are illustrated. Case studies are implemented on the California Independent System Operator (CAISO) electricity market data for a two years period. The proposed methods are evaluated and neural networks showed promising results in predicting the exact values of the gap.