Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeThe option pricing model based on time values: an application of the universal approximation theory on unbounded domains

Paper and Code

Oct 02, 2019

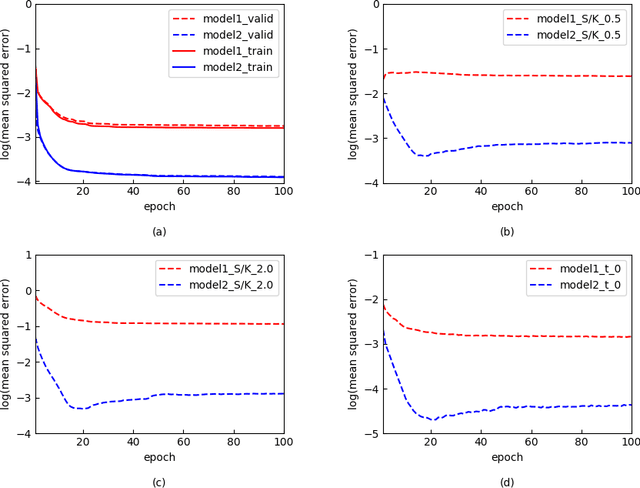

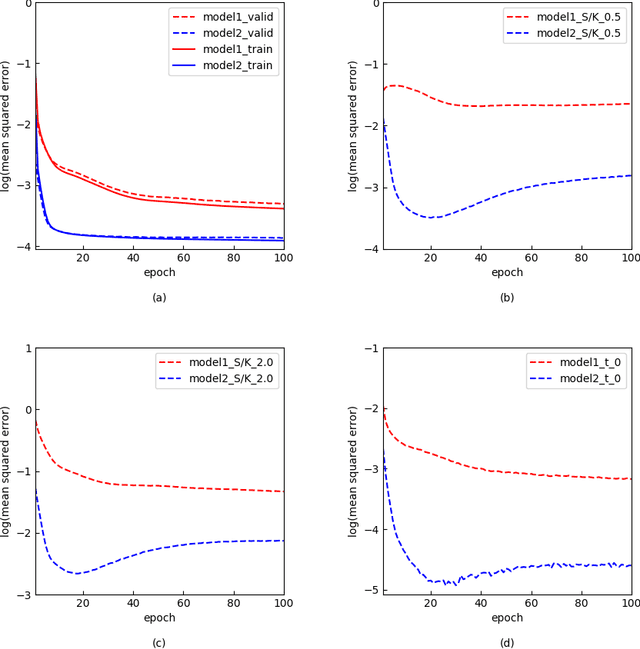

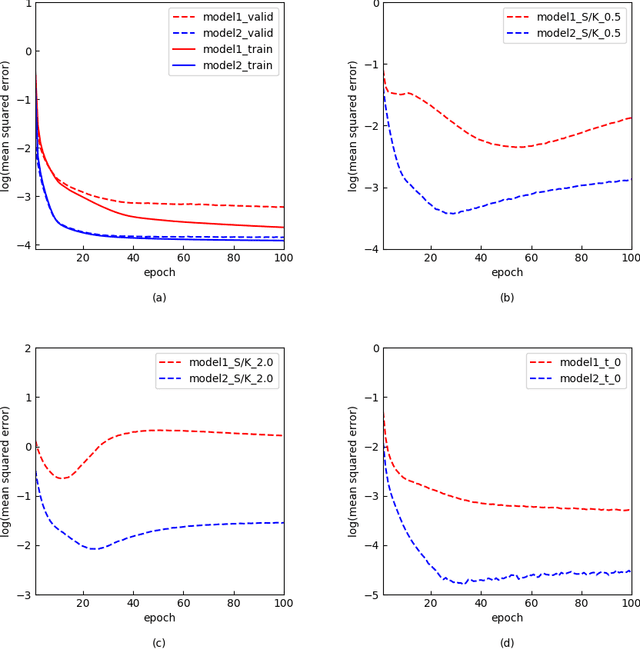

Hutchinson, Lo and Poggio raised the question that if learning works can learn the Black-Scholes formula, and they proposed the network mapping the ratio of underlying price to strike $S_t/K$ and the time to maturity $\tau$ directly into the ratio of option price to strike $C_t/K$. In this paper we propose a novel descision function and study the network mapping $S_t/K$ and $\tau$ into the ratio of time value to strike $V_t/K$. Time values' appearance in artificial intelligence fits into traders' natural intelligence. Empirical experiments will be carried out to demonstrate that it significantly improves Hutchinson-Lo-Poggio's original model by faster learning and better generalization performance. In order to take a conceptual viewpoint and to prove that $V_t/K$ but not $C_t/K$ can be approximated by superpositions of logistic functions on its domain of definition, we work on the theory of universal approximation on unbounded domains. We prove some general results which imply that an artificial neural network with a single hidden layer and sigmoid activation represents no function in $L^{p}(\RR^2 \times [0, 1]^{n})$ unless it is constant zero, and that an artificial neural network with a single hidden layer and logistic activation is a universal approximator of $L^{2}(\RR \times [0, 1]^{n})$. Our work partially generalizes Cybenko's fundamental universal approximation theorem on the unit hypercube $[0, 1]^{n}$.