Get our free extension to see links to code for papers anywhere online!Free add-on: code for papers everywhere!Free add-on: See code for papers anywhere!

Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeStructured low-rank matrix completion for forecasting in time series analysis

Paper and Code

Feb 22, 2018

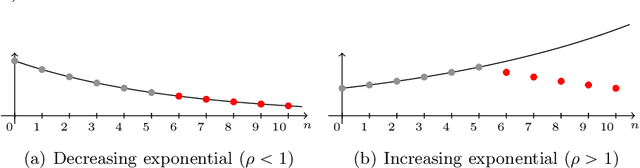

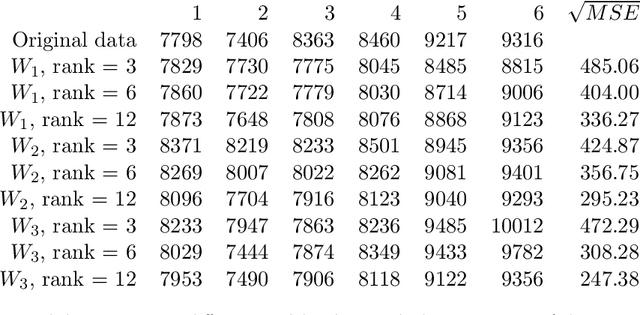

In this paper we consider the low-rank matrix completion problem with specific application to forecasting in time series analysis. Briefly, the low-rank matrix completion problem is the problem of imputing missing values of a matrix under a rank constraint. We consider a matrix completion problem for Hankel matrices and a convex relaxation based on the nuclear norm. Based on new theoretical results and a number of numerical and real examples, we investigate the cases when the proposed approach can work. Our results highlight the importance of choosing a proper weighting scheme for the known observations.

* 25 pages, 12 figures

View paper on