Get our free extension to see links to code for papers anywhere online!Free add-on: code for papers everywhere!Free add-on: See code for papers anywhere!

Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeModeling Volatility and Dependence of European Carbon and Energy Prices

Paper and Code

Aug 30, 2022

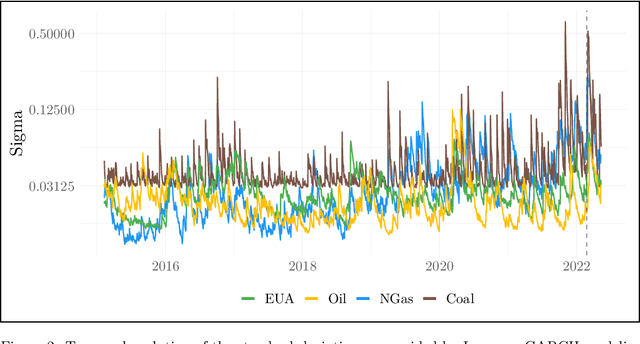

We study the prices of European Emission Allowances (EUA), whereby we analyze their uncertainty and dependencies on related energy markets. We propose a probabilistic multivariate conditional time series model that exploits key characteristics of the data. The forecasting performance of the proposed model and various competing models is evaluated in an extensive rolling window forecasting study, covering almost two years out-of-sample. Thereby, we forecast 30-steps ahead. The accuracy of the multivariate probabilistic forecasts is assessed by the energy score. We discuss our findings focusing on volatility spillovers and time-varying correlations, also in view of the Russian invasion of Ukraine.

View paper on