Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeML-Based Bidding Price Prediction for Pay-As-Bid Ancillary Services Markets: A Use Case in the German Control Reserve Market

Paper and Code

Mar 21, 2025

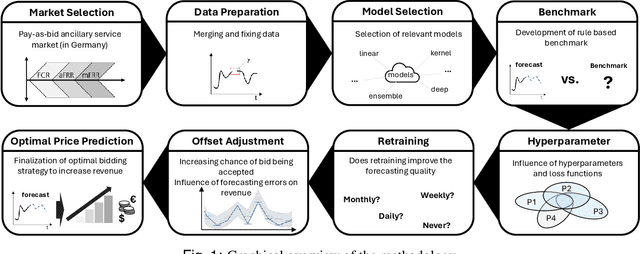

The increasing integration of renewable energy sources has led to greater volatility and unpredictability in electricity generation, posing challenges to grid stability. Ancillary service markets, such as the German control reserve market, allow industrial consumers and producers to offer flexibility in their power consumption or generation, contributing to grid stability while earning additional income. However, many participants use simple bidding strategies that may not maximize their revenues. This paper presents a methodology for forecasting bidding prices in pay-as-bid ancillary service markets, focusing on the German control reserve market. We evaluate various machine learning models, including Support Vector Regression, Decision Trees, and k-Nearest Neighbors, and compare their performance against benchmark models. To address the asymmetry in the revenue function of pay-as-bid markets, we introduce an offset adjustment technique that enhances the practical applicability of the forecasting models. Our analysis demonstrates that the proposed approach improves potential revenues by 27.43 % to 37.31 % compared to baseline models. When analyzing the relationship between the model forecasting errors and the revenue, a negative correlation is measured for three markets; according to the results, a reduction of 1 EUR/MW model price forecasting error (MAE) statistically leads to a yearly revenue increase between 483 EUR/MW and 3,631 EUR/MW. The proposed methodology enables industrial participants to optimize their bidding strategies, leading to increased earnings and contributing to the efficiency and stability of the electrical grid.