Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeLearning the Trading Algorithm in Simulated Markets with Non-stationary Continuum Bandits

Paper and Code

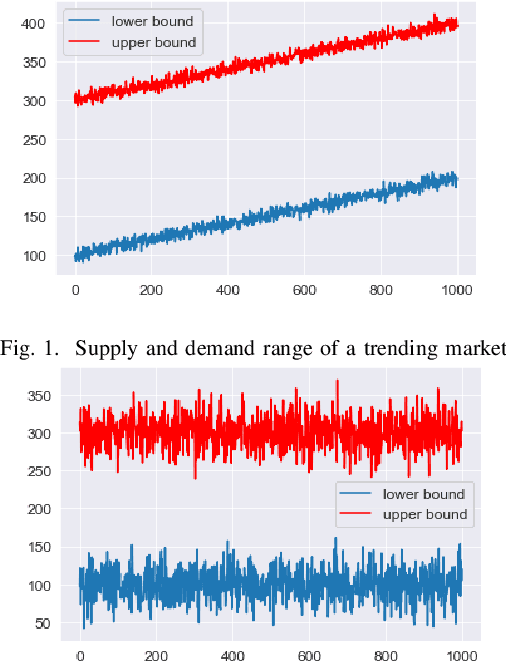

The basic Multi-Armed Bandits (MABs) problem is trying to maximize the rewards obtained from bandits with different unknown probability distributions of payoff for pulling different arms, given that only a finite number of attempts can be made. When studying trading algorithms in the market, we are looking at one of the most complex variants of MABs problems, namely the Non-stationary Continuum Bandits (NCBs) problem. The Bristol Stock Exchange (BSE) is a simple simulation of an electronic financial exchange based on a continuous double auction running via a limit order book. The market can be populated by automated trader agents with different trading algorithms. Within them, the PRSH algorithm embodies some basic ideas for solving NCBs problems. However, it faces the difficulty to adjust hyperparameters and adapt to changes in complex market conditions. We propose a new algorithm called PRB, which solves Continuum Bandits problem by Bayesian optimization, and solves Non-stationary Bandits problem by a novel "bandit-over-bandit" framework. With BSE, we use as many kinds of trader agents as possible to simulate the real market environment under two different market dynamics. We then examine the optimal hyperparameters of the PRSH algorithm and the PRB algorithm under different market dynamics respectively. Finally, by having trader agents using both algorithms trade in the market at the same time, we demonstrate that the PRB algorithm has better performance than the PRSH algorithm under both market dynamics. In particular, we perform rigorous hypothesis testing on all experimental results to ensure their correctness.