Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeEnsemble Sales Forecasting Study in Semiconductor Industry

Paper and Code

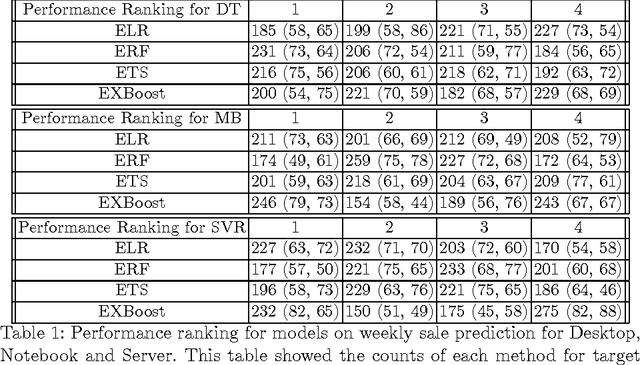

Sales forecasting plays a prominent role in business planning and business strategy. The value and importance of advance information is a cornerstone of planning activity, and a well-set forecast goal can guide sale-force more efficiently. In this paper CPU sales forecasting of Intel Corporation, a multinational semiconductor industry, was considered. Past sale, future booking, exchange rates, Gross domestic product (GDP) forecasting, seasonality and other indicators were innovatively incorporated into the quantitative modeling. Benefit from the recent advances in computation power and software development, millions of models built upon multiple regressions, time series analysis, random forest and boosting tree were executed in parallel. The models with smaller validation errors were selected to form the ensemble model. To better capture the distinct characteristics, forecasting models were implemented at lead time and lines of business level. The moving windows validation process automatically selected the models which closely represent current market condition. The weekly cadence forecasting schema allowed the model to response effectively to market fluctuation. Generic variable importance analysis was also developed to increase the model interpretability. Rather than assuming fixed distribution, this non-parametric permutation variable importance analysis provided a general framework across methods to evaluate the variable importance. This variable importance framework can further extend to classification problem by modifying the mean absolute percentage error(MAPE) into misclassify error. Please find the demo code at : https://github.com/qx0731/ensemble_forecast_methods