Get our free extension to see links to code for papers anywhere online!Free add-on: code for papers everywhere!Free add-on: See code for papers anywhere!

Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeEfficient and robust calibration of the Heston option pricing model for American options using an improved Cuckoo Search Algorithm

Paper and Code

Jul 31, 2015

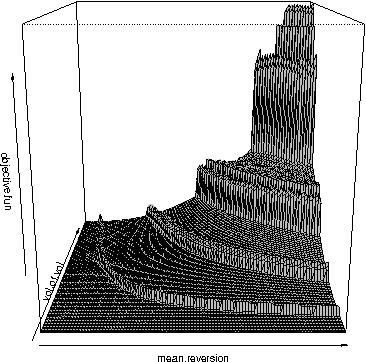

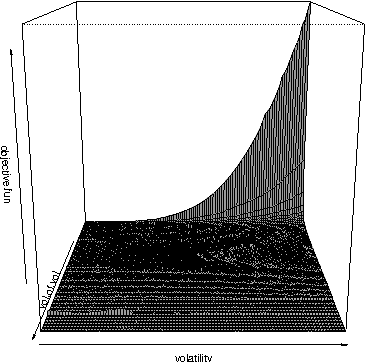

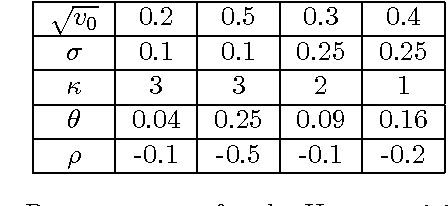

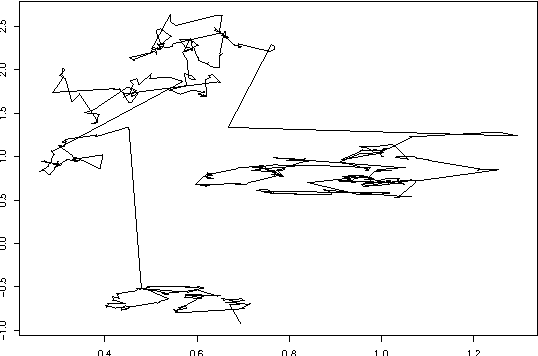

In this paper an improved Cuckoo Search Algorithm is developed to allow for an efficient and robust calibration of the Heston option pricing model for American options. Calibration of stochastic volatility models like the Heston is significantly harder than classical option pricing models as more parameters have to be estimated. The difficult task of calibrating one of these models to American Put options data is the main objective of this paper. Numerical results are shown to substantiate the suitability of the chosen method to tackle this problem.

View paper on