Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeDynamics of Stochastic Momentum Methods on Large-scale, Quadratic Models

Paper and Code

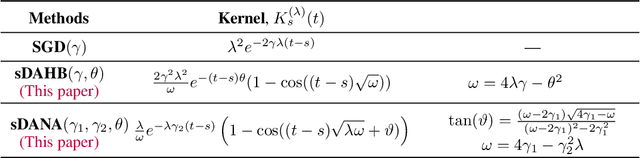

We analyze a class of stochastic gradient algorithms with momentum on a high-dimensional random least squares problem. Our framework, inspired by random matrix theory, provides an exact (deterministic) characterization for the sequence of loss values produced by these algorithms which is expressed only in terms of the eigenvalues of the Hessian. This leads to simple expressions for nearly-optimal hyperparameters, a description of the limiting neighborhood, and average-case complexity. As a consequence, we show that (small-batch) stochastic heavy-ball momentum with a fixed momentum parameter provides no actual performance improvement over SGD when step sizes are adjusted correctly. For contrast, in the non-strongly convex setting, it is possible to get a large improvement over SGD using momentum. By introducing hyperparameters that depend on the number of samples, we propose a new algorithm sDANA (stochastic dimension adjusted Nesterov acceleration) which obtains an asymptotically optimal average-case complexity while remaining linearly convergent in the strongly convex setting without adjusting parameters.