Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeDeepHAM: A Global Solution Method for Heterogeneous Agent Models with Aggregate Shocks

Paper and Code

Dec 29, 2021

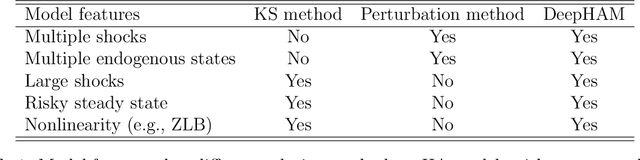

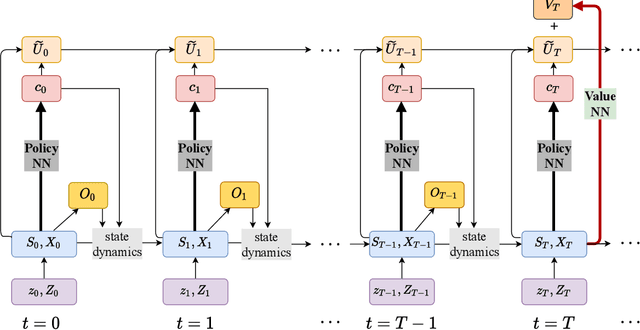

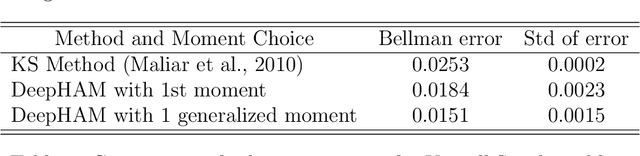

We propose an efficient, reliable, and interpretable global solution method, $\textit{Deep learning-based algorithm for Heterogeneous Agent Models, DeepHAM}$, for solving high dimensional heterogeneous agent models with aggregate shocks. The state distribution is approximately represented by a set of optimal generalized moments. Deep neural networks are used to approximate the value and policy functions, and the objective is optimized over directly simulated paths. Besides being an accurate global solver, this method has three additional features. First, it is computationally efficient for solving complex heterogeneous agent models, and it does not suffer from the curse of dimensionality. Second, it provides a general and interpretable representation of the distribution over individual states; and this is important for addressing the classical question of whether and how heterogeneity matters in macroeconomics. Third, it solves the constrained efficiency problem as easily as the competitive equilibrium, and this opens up new possibilities for studying optimal monetary and fiscal policies in heterogeneous agent models with aggregate shocks.