Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeCRPS Learning

Paper and Code

Feb 01, 2021

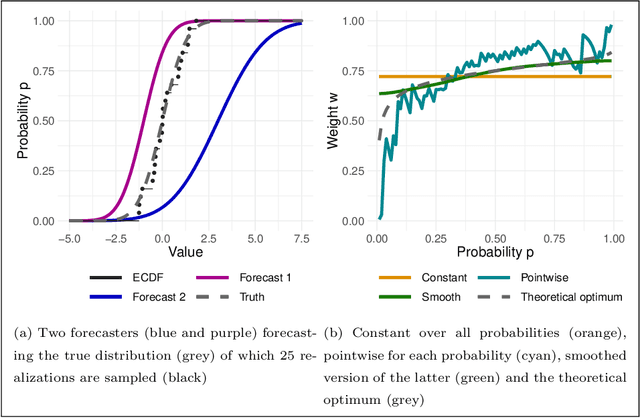

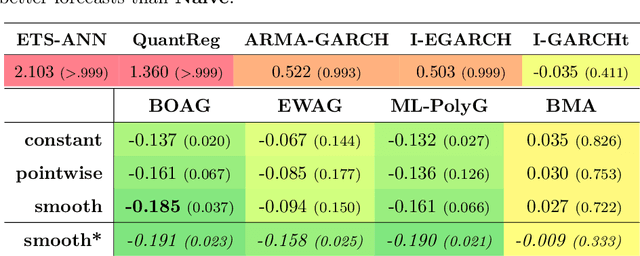

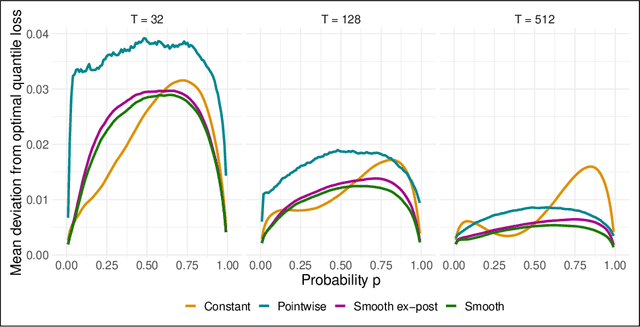

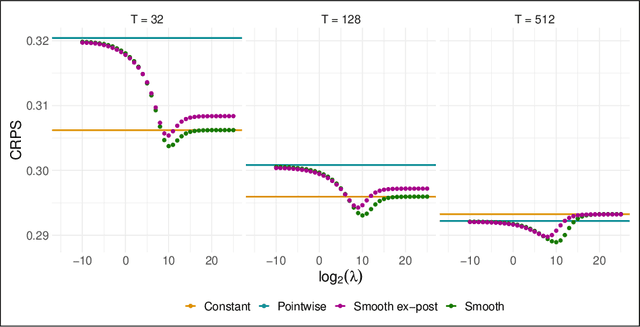

Combination and aggregation techniques can improve forecast accuracy substantially. This also holds for probabilistic forecasting methods where full predictive distributions are combined. There are several time-varying and adaptive weighting schemes like Bayesian model averaging (BMA). However, the performance of different forecasters may vary not only over time but also in parts of the distribution. So one may be more accurate in the center of the distributions, and other ones perform better in predicting the distribution's tails. Consequently, we introduce a new weighting procedure that considers both varying performance across time and the distribution. We discuss pointwise online aggregation algorithms that optimize with respect to the continuous ranked probability score (CRPS). After analyzing the theoretical properties of a fully adaptive Bernstein online aggregation (BOA) method, we introduce smoothing procedures for pointwise CRPS learning. The properties are confirmed and discussed using simulation studies. Additionally, we illustrate the performance in a forecasting study for carbon markets. In detail, we predict the distribution of European emission allowance prices.