Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeCost-Control in Display Advertising: Theory vs Practice

Paper and Code

Sep 05, 2024

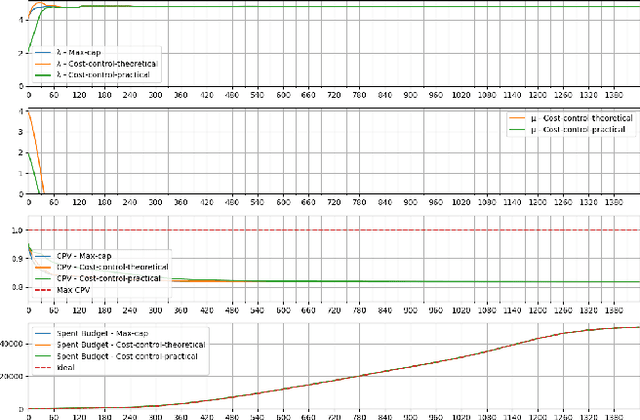

In display advertising, advertisers want to achieve a marketing objective with constraints on budget and cost-per-outcome. This is usually formulated as an optimization problem that maximizes the total utility under constraints. The optimization is carried out in an online fashion in the dual space - for an incoming Ad auction, a bid is placed using an optimal bidding formula, assuming optimal values for the dual variables; based on the outcome of the previous auctions, the dual variables are updated in an online fashion. While this approach is theoretically sound, in practice, the dual variables are not optimal from the beginning, but rather converge over time. Specifically, for the cost-constraint, the convergence is asymptotic. As a result, we find that cost-control is ineffective. In this work, we analyse the shortcomings of the optimal bidding formula and propose a modification that deviates from the theoretical derivation. We simulate various practical scenarios and study the cost-control behaviors of the two algorithms. Through a large-scale evaluation on the real-word data, we show that the proposed modification reduces the cost violations by 50%, thereby achieving a better cost-control than the theoretical bidding formula.