Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeComputing the optimal distributionally-robust strategy to commit to

Paper and Code

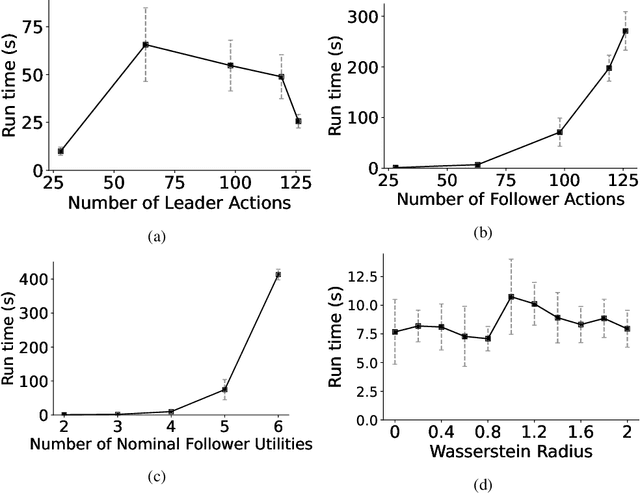

The Stackelberg game model, where a leader commits to a strategy and the follower best responds, has found widespread application, particularly to security problems. In the security setting, the goal is for the leader to compute an optimal strategy to commit to, in order to protect some asset. In many of these applications, the parameters of the follower utility model are not known with certainty. Distributionally-robust optimization addresses this issue by allowing a distribution over possible model parameters, where this distribution comes from a set of possible distributions. The goal is to maximize the expected utility with respect to the worst-case distribution. We initiate the study of distributionally-robust models for computing the optimal strategy to commit to. We consider the case of normal-form games with uncertainty about the follower utility model. Our main theoretical result is to show that a distributionally-robust Stackelberg equilibrium always exists across a wide array of uncertainty models. For the case of a finite set of possible follower utility functions we present two algorithms to compute a distributionally-robust strong Stackelberg equilibrium (DRSSE) using mathematical programs. Next, in the general case where there is an infinite number of possible follower utility functions and the uncertainty is represented by a Wasserstein ball around a finitely-supported nominal distribution, we give an incremental mixed-integer-programming-based algorithm for computing the optimal distributionally-robust strategy. Experiments substantiate the tractability of our algorithm on a classical Stackelberg game, showing that our approach scales to medium-sized games.