Get our free extension to see links to code for papers anywhere online!Free add-on: code for papers everywhere!Free add-on: See code for papers anywhere!

Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeAn Evolutionary Optimization Approach to Risk Parity Portfolio Selection

Paper and Code

Jan 19, 2015

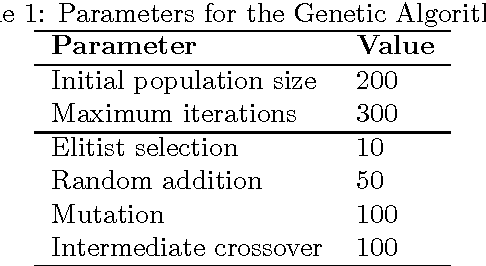

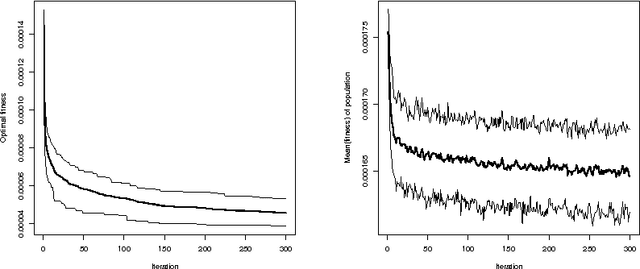

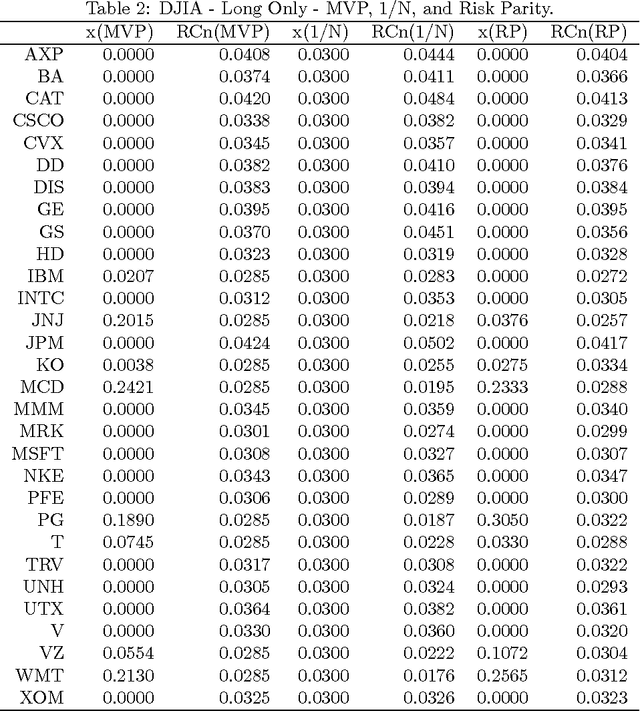

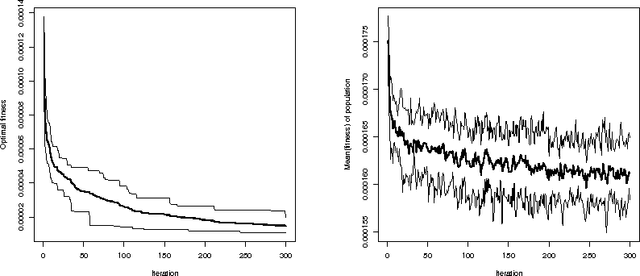

In this paper we present an evolutionary optimization approach to solve the risk parity portfolio selection problem. While there exist convex optimization approaches to solve this problem when long-only portfolios are considered, the optimization problem becomes non-trivial in the long-short case. To solve this problem, we propose a genetic algorithm as well as a local search heuristic. This algorithmic framework is able to compute solutions successfully. Numerical results using real-world data substantiate the practicability of the approach presented in this paper.

* Lecture Notes in Computer Science Volume 9028: 279-288. 2015

View paper on